The Indian banking sector has undergone a significant transformation in recent years, thanks to the Digital India initiative launched by the Government of India. Digital India has brought about a paradigm shift in the way banking services are delivered to customers, making them more accessible, efficient, and cost-effective. In this article, we’ll explore what digital banking means in the Indian context and how it is transforming the banking landscape.

The Digital India initiative aims to provide every Indian citizen with access to digital infrastructure, digital services, and digital literacy. It seeks to transform India into a digitally empowered society and knowledge economy. The banking sector is an essential component of this transformation, as it is a critical enabler of financial inclusion and economic growth. Digital banking is at the forefront of this transformation, enabling banks to reach out to a larger customer base and provide them with a seamless banking experience.

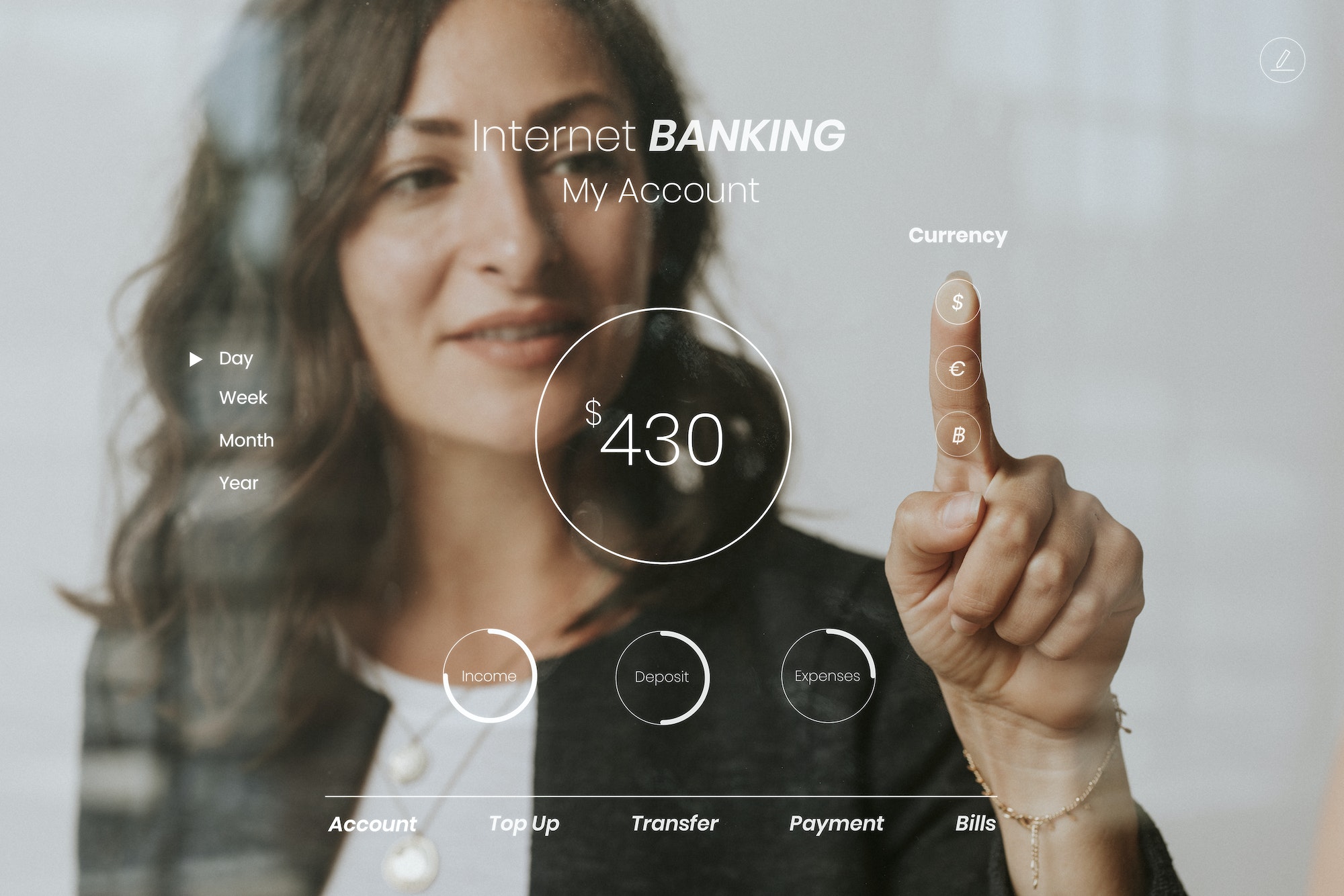

Digital Banking refers to the use of digital channels, such as the internet, mobile phones, and ATMs, to access banking services. It encompasses a wide range of services, such as online banking, mobile banking, digital payments, and e-wallets. Digital banking has made banking more convenient, accessible, and affordable for customers, especially those in rural and remote areas. It has also enabled banks to reduce their operational costs and improve their efficiency.

Digital banking has brought about several benefits for customers, such as:

It goes without saying that the advantages much exceed the expenses of advancing to a more technologically advanced method of doing things. Likewise, digital banking as a technology byproduct attempts to simplify the lives of bank clients. Digital banking offers the following advantages:

- Convenience: Digital banking allows customers to access banking services anytime and anywhere, without having to visit a bank branch.

- Cost-effectiveness: Digital banking eliminates the need for customers to travel to a bank branch, reducing their transportation costs.

- Accessibility: Digital banking enables customers in remote and rural areas to access banking services without having to travel long distances.

- Speed: Digital banking allows customers to perform transactions quickly and efficiently, without having to wait in long queues at bank branches.

Digital banking has also brought about several benefits for banks, such as:

- Cost savings: Digital banking has enabled banks to reduce their operational costs by automating several processes.

- Improved efficiency: Digital banking has made it easier for banks to manage their operations, reducing the time and effort required to perform various tasks.

- Increased customer engagement: Digital banking has enabled banks to engage with their customers more effectively, providing them with personalised services and solutions.

- Improved risk management: Digital banking has enabled banks to better manage their risks by providing them with real-time data and analytics.

Digital banking has transformed the Indian banking landscape, making it more competitive and customer-centric. Banks are now using digital technologies to offer innovative products and services, such as instant loans, digital wallets, and robo-advisory services. These services are aimed at meeting the evolving needs of customers and providing them with a superior banking experience.

However, there are several challenges associated with digital banking that need to be addressed. One of the biggest challenges is the digital divide, which refers to the gap between those who have access to digital technologies and those who do not. This divide is particularly pronounced in rural and remote areas, where access to digital infrastructure is limited. To bridge this divide, banks need to work with the government to provide digital infrastructure and literacy to remote areas.

Another challenge is cybersecurity, as digital banking has made banks more vulnerable to cyber-attacks. Banks need to invest in robust cybersecurity measures to protect their systems and data from cyber threats. They also need to educate their customers about cybersecurity best practices and provide them with the necessary tools and resources to protect their data.

Digital banking payment types

Banking cards: Not only are banking cards used to withdraw cash, but they also permit various types of digital payment. Cards may be used for both online and Point of Sale (PoS) purchases. Banks may also provide prepaid cards; these cards are not tied to a bank account, but operate based on the funds deposited onto them.

Unstructured Supplemental Service Data (USSD): Mobile transactions may be conducted without an application and internet connection by calling *99#. The number is applicable nationally and supports greater financial inclusion at the local level. The service allows the caller to navigate a voice-activated menu and choose the required choice on the mobile screen. The sole restriction is that the caller’s cell phone must be associated with the specified bank account.

Aadhaar Enabled Payment System (AEPS): AEPS enables the customer to begin banking instructions upon successful Aadhaar verification.

Unified Payments Interface (UPI): UPI is now the most popular type of digital banking. UPI utilises a virtual payment address (VPA) so that the user may transfer cash without providing their bank account information or IFSC code. The applications of UPI allow you to unify all of your bank accounts into an one location. Transfers and receipts of funds are available around the clock, with no time constraints. In India, the UPI-based applications include BHIM, PhonePe, and Google Pay. In addition to transferring payments to other virtual addresses and bank accounts, the BHIM application allows the user to transfer monies to another Aadhaar number. Additionally, UPI-based payments are costless.

Mobile Wallets: Mobile wallets have removed the need to memorise four-digit card PINs, input CVV information, and carry currency. Mobile wallets hold bank account and card details so that users may simply add money to the wallet and pay other businesses using similar programmes. Popular mobile wallets include Paytm, Freecharge, and Mobiwik, among others. However, mobile wallets often have a restriction on the amount that may be put. A minor fee may also be assessed when transferring money from a mobile wallet to a bank account.

PoS terminals: They are typically portable devices that read a card for payment authorization and completion. The majority of supermarkets and petrol stations accept this form of payment. As digital banking has flourished, however, PoS terminals have developed into more than physical PoS devices. Virtual and Mobile PoS terminals have emerged, which use the NFC technology of mobile phones and web-based payment apps to begin transactions.

Internet and Mobile Banking: Internet banking, often known as e-banking, refers to accessing some banking services, such as financial transfers and account opening and closure, through the internet. Internet banking is a subset of digital banking since it is confined to basic tasks alone. Likewise, mobile banking is the provision of financial services using mobile-based apps.

Future of Electronic Banking

According to a Deloitte study report on must-haves for a completely digital bank, any bank aspiring to go fully digital must have the following as the major success drivers:

1. Option to purchase currency

2. Personalised standing choices

3. Accounts associated with tax exemption status 4. Card blocking function

5. advancements in safety vaults

6. Incorporation of stock exchange investment channels

7. Analytical financial management

8. Permit the aggregation of accounts from several banks

9. Quickly available aid

In conclusion, digital banking has transformed the Indian banking landscape, making banking more accessible, efficient, and cost-effective for customers. It has enabled banks to offer innovative products and services, improve their efficiency, and engage with their customers more effectively. However, there are also challenges associated with digital banking, such as the digital divide and cybersecurity risks, that need to be addressed. Banks need to work with the government to bridge the digital divide and invest in robust cybersecurity measures to protect their systems and data. Despite these challenges, digital banking has the potential to transform the Indian economy and promote financial inclusion, making banking services accessible to all. As we move forward, it is essential to continue to leverage digital technologies to build a more inclusive and prosperous India.